The AI Cloud Wars and the Energy Crunch: Infrastructure at a Breaking Point July 2026

The global cloud computing market has official broken past the $1 trillion threshold. Driven entirely by the relentless demands of generative AI, specialized agentic workflows, and multi-trillion parameter model deployments, a fierce battle is raging.

The traditional cloud paradigm is shifting. It is no longer just about who has the best software ecosystem; it is a brutal logistical war over two physical constraints: GPU allocation and gigawatts of electricity.

This extensive guide explores the two biggest stories shaping tech today: the five-way battle of the 2026 AI Cloud Wars and the massive energy crisis threatening to halt AI scaling entirely.

Part 1: The AI Cloud Wars — Hyperscalers vs. The Neoclouds

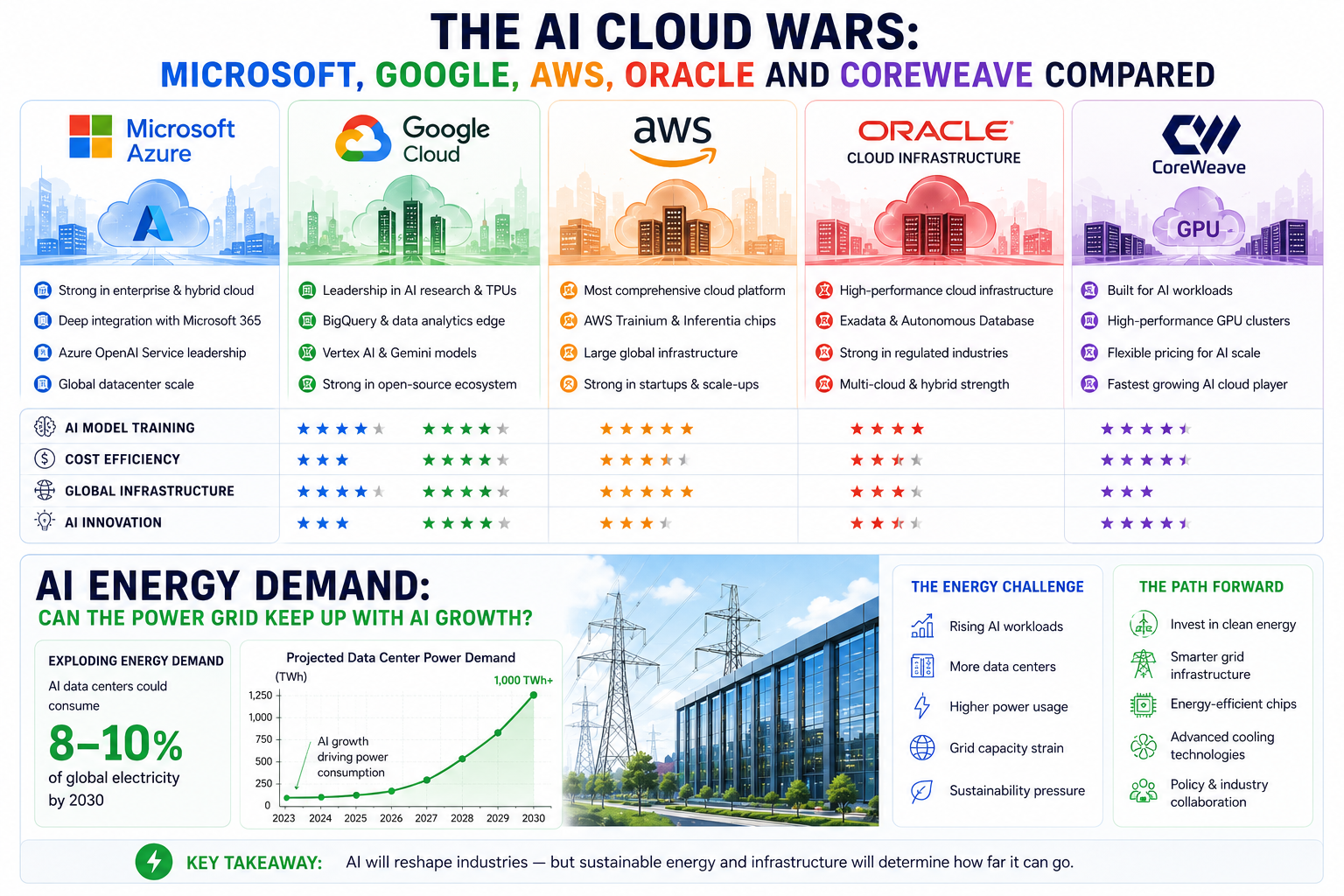

The cloud architecture of July 2026 is starkly divided. On one side stand the Trillion-Dollar Hyperscalers (Microsoft, Google, AWS), who are aggressively trying to retrofit legacy infrastructure. On the other side are the nimble, AI-native upstarts and legacy database giants (CoreWeave, Oracle) stealing market share by offering bare-metal, high-density environments.

1. Microsoft Azure: The Enterprise Cohort Leader

Holding roughly 25% of the global cloud market, Microsoft Azure remains the primary home for frontier-class enterprise AI.

The Edge: Azure’s unmatched advantage is its exclusive, deep integration with OpenAI’s production models.

The Reality: Azure has faced intense capacity bottlenecks. To keep up with OpenAI’s massive computing needs, Microsoft has had to execute massive "cap-ex offloading," aggressively leasing data center capacity from specialized third parties to bridge its infrastructure shortages.

2. Google Cloud Platform (GCP): The Sovereign Vertical King

Google Cloud has surged aggressively in growth, capturing roughly 11% of the market but dominating in performance efficiency.

The Edge: Google is the most vertically integrated player in the world. While competitors are at the mercy of semiconductor supply chains, Google deploys its custom TPU v6 (Trillium) chips at massive scale.

The Strategy: For multi-modal processing and massive token context windows (like Gemini 3.5 Pro), GCP is structurally cheaper and more optimized than any framework built purely on generalized hardware.

3. Amazon Web Services (AWS): The Cost-Per-Token Disruptor

AWS still retains the largest overall cloud market share at 31%, though it faces intense pressure from AI-first workloads.

The Edge: AWS has democratized custom chips via Trainium 3 and Inferentia 2, skipping the steep third-party hardware markups.

The Strategy: Through Amazon Bedrock, AWS targets companies building localized, highly scaled agent workflows that prioritize low cost-per-token over chasing raw frontier intelligence benchmarks.

4. Oracle Cloud Infrastructure (OCI): The Dark Horse of AI Core Infrastructure

Oracle has pulled off one of the greatest turnarounds in tech history, cementing itself as a tier-1 AI cloud destination.

The Edge: Oracle realized early that AI training requires raw speed, not generalized virtualization overhead. OCI offers pure, bare-metal clusters linked together with ultra-low latency RDMA networks.

The Momentum: Oracle’s massive backlog has ballooned to historic highs. Tech leaders—including Microsoft and OpenAI—regularly contract Oracle to build out custom, physical AI clusters when their own footprints hit capacity limits.

5. CoreWeave: The Specialized "Neocloud" Powerhouse

From a niche GPU mining operation to a near top-10 global cloud vendor generating billions in quarterly revenue, CoreWeave is the ultimate "GPUaaS" (GPU-as-a-Service) disrupter.

The Edge: Speed and execution. CoreWeave does not host web servers or basic databases. It builds data centers strictly for high-density AI clusters. While a hyperscaler takes 2–4 years to build a campus, CoreWeave can spin up tens of thousands of cluster-mapped GPUs in weeks.

The Backing: Backed by multibillion-dollar asset-backed debt structures and direct, priority allocations from hardware manufacturers, CoreWeave acts as the essential infrastructure pipeline for labs like Mistral AI and OpenAI.

Part 2: AI Energy Demand — Can the Power Grid Survive?

As cloud providers race to build out millions of new GPUs, they are crashing hard into a physical brick wall: The Global Power Grid.

According to recent data from Gartner, worldwide data center electricity consumption is projected to spike 26% in 2026 alone, reaching 565 Terawatt-hours (TWh). By 2030, that number is expected to balloon past 1,200 TWh—exceeding the entire energy consumption of nations like Japan.

The Physics of the Problem: Training vs. Inference

Historically, training large frontier models was considered the main energy drain. In 2026, the paradigm has flipped. Inference (running the models live for users) now accounts for 80% to 90% of total AI energy draw.

A traditional Google keyword search uses a tiny fraction of a watt-hour.

A single complex reasoning query on a advanced generative model can pull nearly 10x that amount of electricity.

Multiply that by billions of queries daily from autonomous agents, and data centers are requiring 100 MW to 750 MW of power per site.

The High-Density Legacy Wall

Standard enterprise data centers built over the last decade were engineered to handle 10 to 15 kilowatts (kW) per server rack.

A single modern AI high-density rack (such as the NVIDIA Blackwell systems) draws between 120 kW and 140 kW. Attempting to run these setups on legacy infrastructure melts standard air-cooling systems. As a result, 2026 has made direct-to-chip liquid cooling mandatory for all newly constructed facilities.How Tech Giants Are Sourcing Power in 2026

Faced with overtaxed public utility grids, cloud providers are taking energy production into their own hands:

┌───► 1. Small Modular Reactors (SMRs) & Nuclear Deals

│ (Long-term baseline power for massive campuses)

│

AI POWER STRATEGY ├───► 2. Natural Gas Turbines & Co-location

(Mid-2026 Tech) │ (Fastest deployment method; deployed in 12–18 months)

│

└───► 3. Flexible Grid Optimization via Code

(Using AI models to predict and utilize idle grid capacity)

The Nuclear Renaissance: Hyperscalers are executing massive power-purchase agreements tied directly to nuclear facilities. Small Modular Reactors (SMRs) have become the holy grail for providing carbon-free, constant "baseload" power directly to data center campuses, bypassing municipal grids entirely.

Natural Gas Bridges: Because nuclear and grid overhauls take years, natural gas has become the emergency bridge. Cloud vendors are increasingly building on-site natural gas generation to bring megawatt-scale sites online within a 12-to-18-month window.

Grid Optimization Software: Leading developers are pairing up with utilities to deploy predictive AI models to manage the grid itself. By utilizing advanced algorithms to shift massive, non-urgent training workloads to off-peak hours when excess renewable energy is high, operators are unlocking hidden capacity out of existing copper infrastructure.

The World Economic Forum

Final Verdict: The Infrastructure Shift of 2026

The true winner of the AI Cloud Wars won't necessarily be the company with the smartest software engineers. The crown will go to whoever secures the physical land, the heavy-duty cooling infrastructure, and the massive electrical capacity needed to sustain the next generation of intelligence.

For developers and enterprises, navigating this space means building resilient multi-cloud architectures—leveraging giants like Google or AWS for standard operations, while leaning on specialized architectures like Oracle and CoreWeave to dodge capacity constraints and optimize your true cost-per-token.

Tags

#AICloud #CloudWars #AIInfrastructure #CloudComputing #AIDataCenters #DataCenters #AIEnergy #PowerGrid #EnergyCrunch #ArtificialIntelligence #GenerativeAI #AI2026 #TechTrends2026 #FutureOfAI #EnterpriseAI #CloudAI #NVIDIA #AmazonAWS #MicrosoftAzure #GoogleCloud #OracleCloud #CoreWeave #OpenAI #Anthropic #GoogleAI #MetaAI #AIChips #Semiconductors #GPU #HighPerformanceComputing #HPC #Compute #AITraining #AIInference #DigitalInfrastructure #DataInfrastructure #Electricity #RenewableEnergy #NuclearEnergy #EnergySecurity #GridModernization #SustainableAI #Technology #Innovation #FutureTech #BusinessTechnology #TechIndustry #DigitalTransformation #AIInvestment #EmergingTech